Chad Rubin

June 24, 2026 · 11 min read

Operator notes by email

Short, opinionated takes on AI agents, Amazon PPC, pricing, and inventory. No fluff. About once a week.

Every Amazon brand at scale eventually gets the same advice. From the agency. From the consultant. From the board. From the friend who sold their brand last year. "You need to diversify off Amazon. Get on Target, get on Walmart, get on Faire, build DTC. Reduce your Amazon concentration risk."

The advice sounds smart. It is also, in most cases, structurally wrong. Not because diversification is bad. Because the standard way of doing it turns your biggest channel into a slave of your smallest one.

I will tell you exactly how that happens. I have lived it. I ran Think Crucial for over a decade, scaled it, watched a hundred peers expand off Amazon, and watched roughly 80% of them end up with worse Amazon margins six months later than they had before they ever opened the second channel. The 20% who got better did it specifically by structuring the expansion to defeat the trap. The other 80% did not understand the trap was there.

This post is the operator's framework for understanding the trap and the four ways to do multi-marketplace expansion without falling into it. The deep-dives in this cluster each take one piece of the framework apart in detail. Read whichever one solves the problem in front of you. Then come back here for the system view.

## Key takeaways >- Amazon scrapes prices from Walmart, Target, your DTC site, and most other public marketplaces. Anything they find that is lower than your Amazon price gets treated as your true price.- When a small channel (5% of revenue) carries a different price than Amazon, that small channel's price becomes your Amazon ceiling. This is the Brand-as-Slave-to-Channel problem.- Most multi-marketplace expansions accidentally create this trap by listing identical UPCs at different prices across channels.- The four ways out: identical price across channels, different SKU/UPC per channel, different pack size per channel, or different brand per channel. Each has trade-offs.- The operator who reads channel expansion as a margin question (not a revenue question) wins. The operator who reads it as a diversification question loses.

The standard pitch for expanding off Amazon is risk reduction. "If Amazon suspends your account, you need somewhere to land." "If Amazon raises fees again, you need a channel where you control the economics." "If the algorithm changes, you need a buffer." All of those statements are true in isolation. Each one is also a setup for the trap.

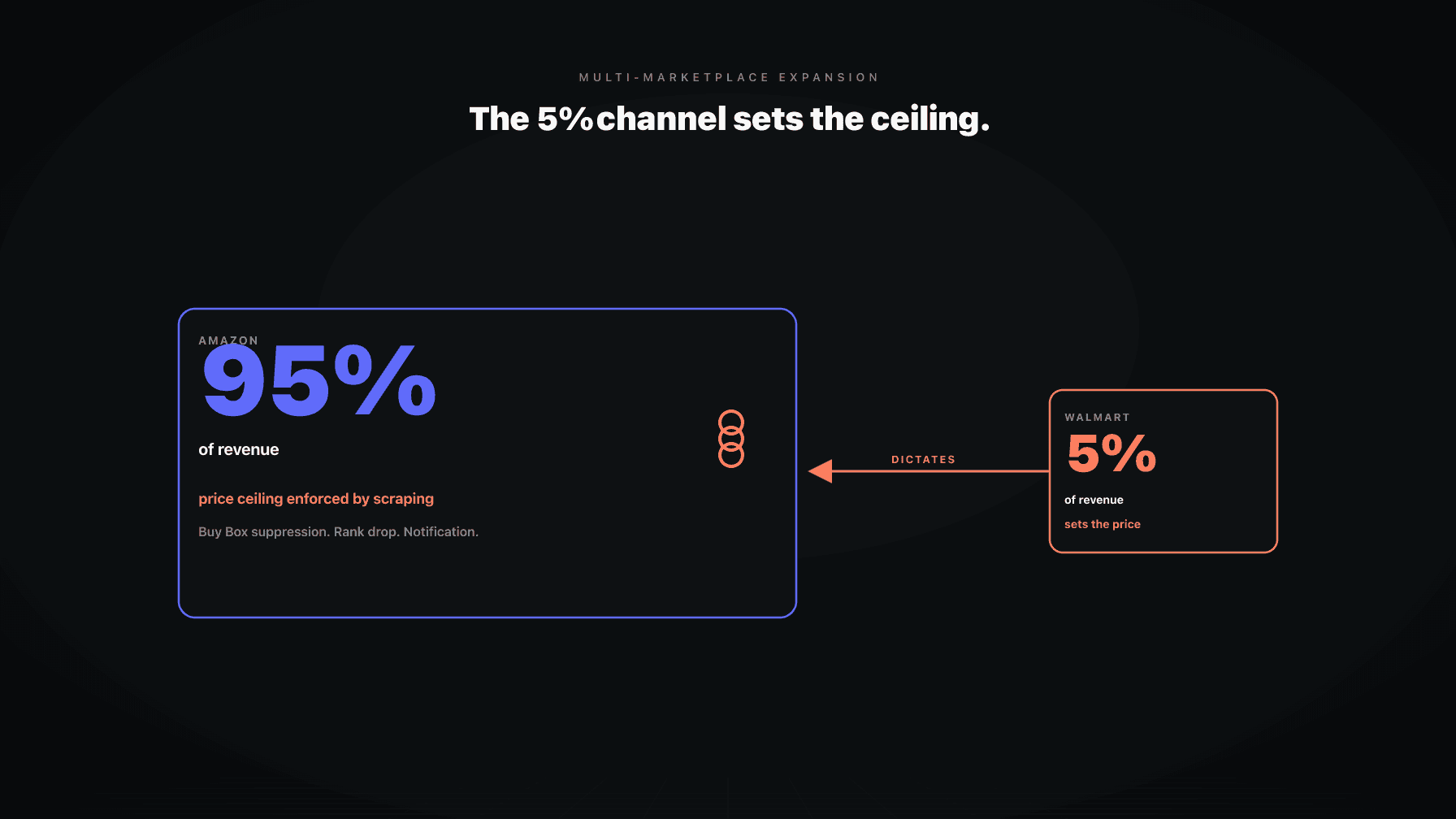

The trap is this: the moment your off-Amazon channel becomes large enough to be useful for risk reduction (let us say 5% of total revenue), it also becomes large enough to be visible to Amazon's pricing systems. Amazon scrapes those systems continuously. The price it finds becomes part of how it evaluates your Amazon listing.

If your Walmart price is lower than your Amazon price, Amazon does one of three things. It suppresses your Buy Box on the Amazon listing. It quietly slides your organic rank because it sees you as overpriced. Or it sends you a "pricing notification" demanding you match the Walmart price on Amazon or face Buy Box loss. The first two are silent. The third is direct. All three turn Walmart into your Amazon ceiling.

From reading to action

If the framework above sounds familiar, your Amazon account is probably carrying the same drag. Apply and we will show what Marko, Oracle, and Bruno would change in your first week.

Ran a 7-figure Amazon brand for a decade. Founded Skubana (acquired). Co-founded Prosper Show. 15+ years on Amazon.

Join the brands that replaced agencies and tools with AI employees.

You did not expand to Walmart to lose your Amazon Buy Box. You expanded to reduce risk. But by listing the same UPC at a lower price on Walmart (because Walmart fees are lower, so you set a lower price to be competitive there), you handed Amazon a cudgel to beat you with. The 95% of your revenue is now a slave to the pricing of the 5%.

I call this the Brand-as-Slave-to-Channel problem. The 5% rule deep-dive covers it in detail. Most operators do not realize they have created the trap until they look at why their Amazon margin dropped after a "safe diversification."

Amazon does not advertise this. They do not have to. Anyone who has run an Amazon brand for 12 months has seen it happen. Amazon's pricing systems scrape Walmart, Target, your DTC site, and most other public marketplaces on a continuous basis. If Amazon finds the same product (same UPC, same parent brand, sometimes same product image) at a lower price elsewhere, it treats that lower price as a signal.

Three things can happen with that signal. The Amazon price-scraping deep-dive covers all three in detail and shows the actual notifications and Buy Box behaviors. Short version:

All three look like Amazon problems. They are not. They are channel-architecture problems you created the day you listed the same UPC at different prices in different places.

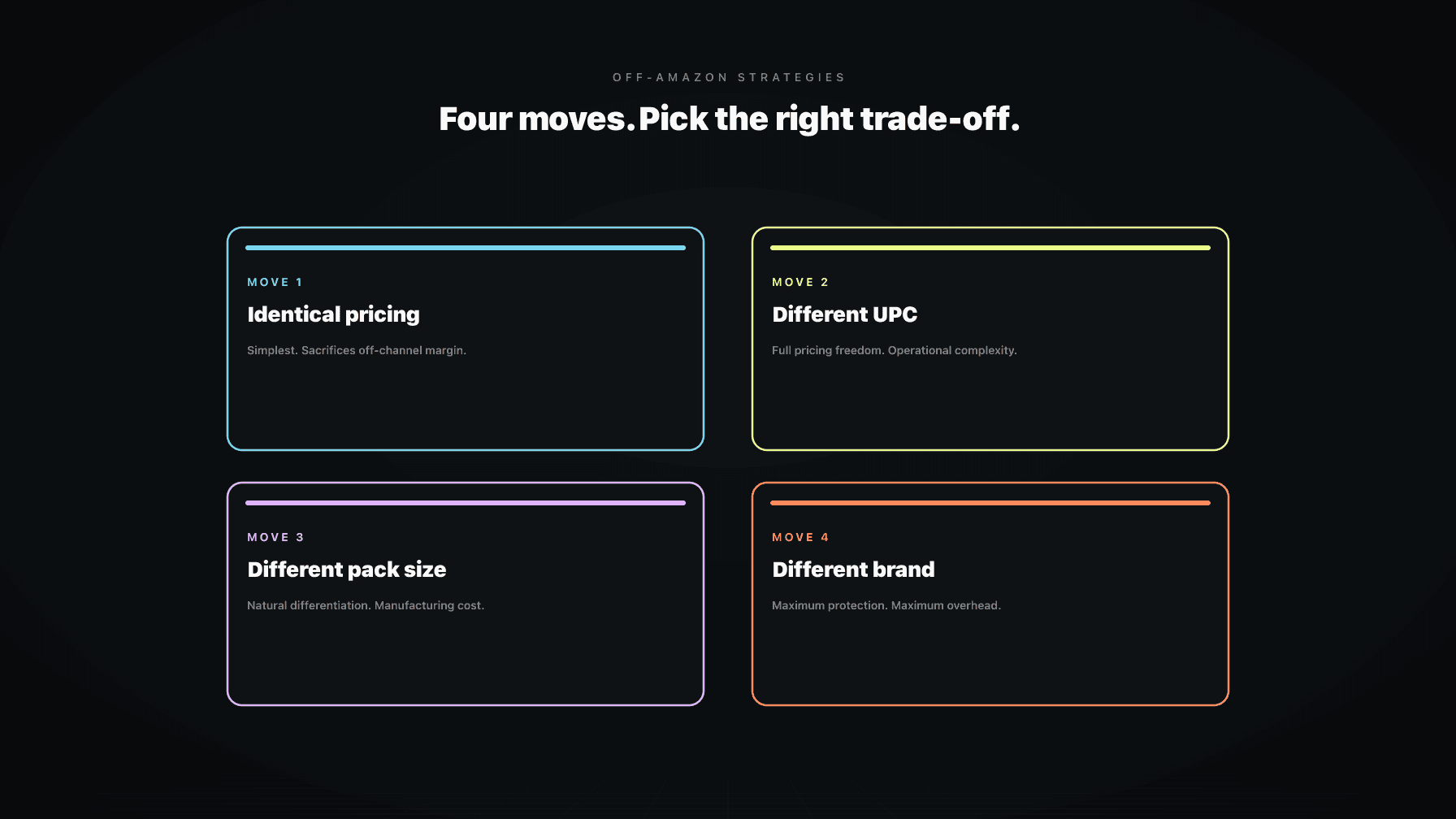

Once you understand the trap exists, the question is how to expand without triggering it. There are exactly four structural moves. Each one has its own trade-offs.

The simplest fix. Pick one price per product and hold it everywhere. Walmart, Amazon, Target, your DTC site, all the same number.

Trade-off: you give up the per-channel pricing optimization that makes some channels actually profitable. Walmart's lower fee structure should let you price lower there and still make margin. If you hold the Amazon price on Walmart, you make more margin per unit on Walmart but you sell fewer units because you are not price-competitive in Walmart's environment.

Who it works for: brands whose Amazon margin is the dominant economic reality and whose off-channel expansion is purely defensive. If Walmart is 5% of revenue and you do not want Amazon to lose 30% of its margin because of it, identical pricing is the safest move.

The structural fix. Walmart sees a different UPC than Amazon sees, on a slightly different version of the product. Amazon's scraping systems do not match the two UPCs to each other and the price difference is invisible.

Trade-off: you carry SKU and inventory complexity for the same physical product. Two UPCs to manage. Two listings to optimize. Two demand forecasts to keep separate. Operational overhead goes up. Done badly, you also lose the brand consolidation benefits of single-SKU multi-channel selling.

Who it works for: brands large enough to absorb the operational complexity. The off-Amazon without breaking margins deep-dive walks the exact UPC structure that works.

A specific case of Move 2. Walmart gets a 2-pack at $19.99. Amazon gets a 3-pack at $27.99. Different UPC because different SKU configuration. Per-unit pricing is similar but the visible price points are different and Amazon's scraping does not flag them as the same product.

Trade-off: you need real product differentiation (different counts, different sizes, different bundle configurations) and you need to manufacture and warehouse multiple configurations. Capex up front. Inventory complexity ongoing.

Who it works for: brands with products that pack-size naturally (supplements, household goods, consumables). Less natural for high-AOV single-unit items.

The maximum-structure fix. The Amazon brand is one company. The Walmart brand is another (different brand name, different parent UPC structure, sometimes different product packaging). To Amazon's systems they are unrelated products.

Trade-off: you are running two brands. Two marketing efforts. Two customer-service streams. Two sets of reviews to build. Two listings to optimize. The cost is real. The protection is also real.

Who it works for: brands at the scale where the off-Amazon channel is going to be 20%+ of revenue and is being built as a real second business, not a risk-reduction lever.

Most brands pick the wrong move because they do not understand which question they are actually answering. Three operator questions sort the right move from the wrong one.

Question 1: What is the off-Amazon channel for?

If it is defensive (we want a place to land if Amazon suspends us), Move 1 (identical pricing) is correct. If it is a real second business intended to grow, Move 4 (different brand) is correct. If it is somewhere in between, Move 2 or 3 is the answer.

Question 2: What is the operational capacity to handle SKU complexity?

A 50-SKU brand running Move 2 (different UPC per channel) is now a 100-SKU brand operationally. Can your team and your tools handle that? If yes, Move 2 is on the table. If no, Move 1 is the only safe option.

Question 3: What is the actual margin difference between channels?

If the margin math means you could earn more on Walmart at a 15% lower price than at the Amazon price, Move 1 is leaving money on the table. If the margin math means Walmart at the Amazon price is roughly break-even anyway, Move 1 is fine and you spend the operational complexity elsewhere.

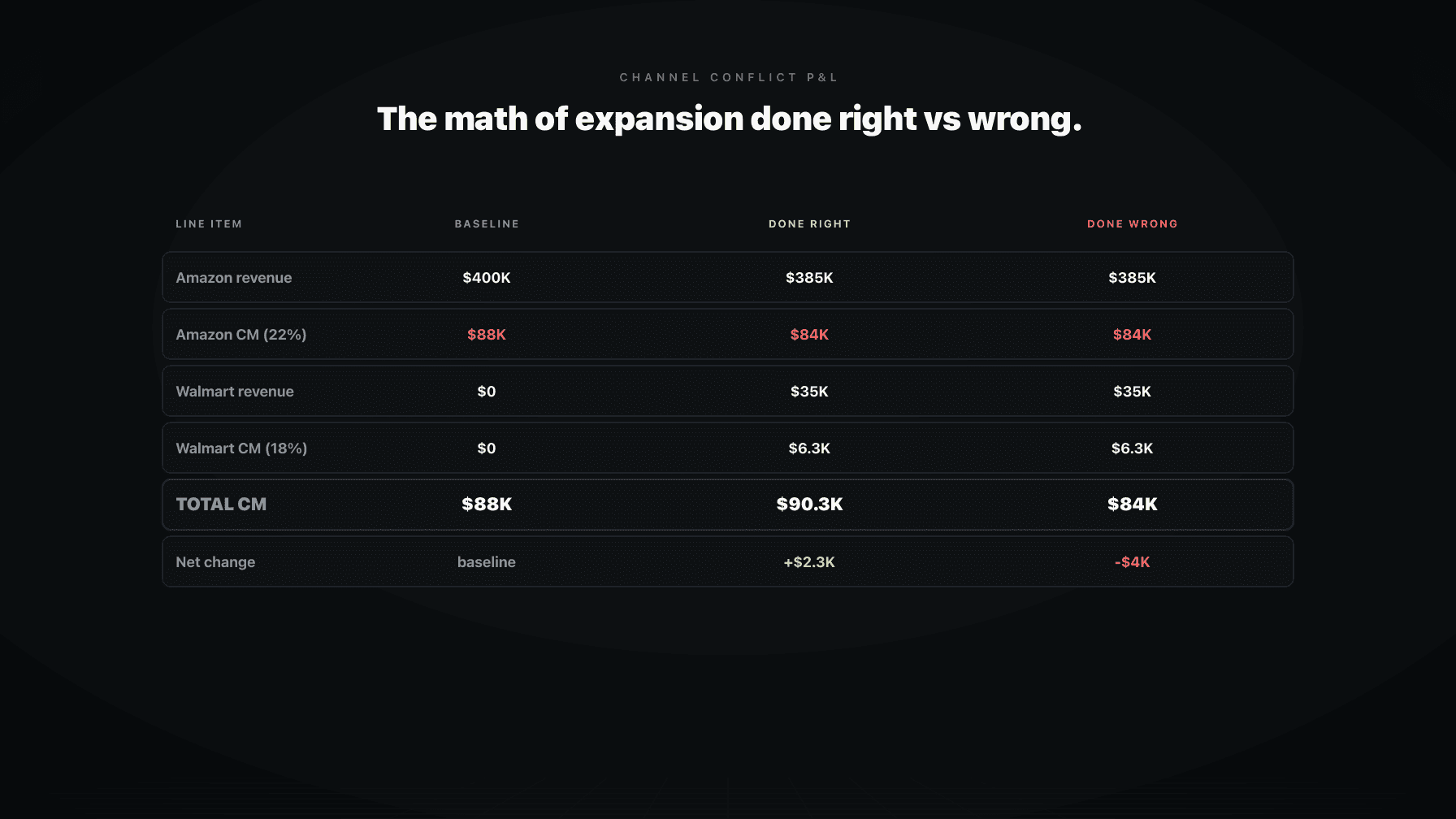

The channel conflict math deep-dive gives you the P&L model to run this analysis on your own brand.

I have seen brands fall into this trap consistently. The pattern is almost always the same.

The board or the agency tells them to diversify. They get on Walmart because it is the obvious next step. The Walmart sales team helps them set up listings. The Walmart team's incentive is volume on Walmart, so they recommend Walmart-competitive pricing (which is below Amazon's pricing because Walmart fees are lower). The brand lists the same UPC at the lower Walmart price. The brand celebrates a successful expansion.

Two months later, the Amazon team notices the Amazon margin has dropped. They cannot figure out why. They blame Amazon fees, the algorithm, the season, the competition. The actual cause is sitting on Walmart. The Walmart price has become the Amazon ceiling and no one in the company has the cross-channel visibility to see it.

This is the operator-level reason single-function tools do not work in multi-channel brands. A repricer that only sees Amazon does not see the Walmart trap. A PPC tool that only sees Amazon does not see why conversion dropped. A demand planner that does not see channel-by-channel margin makes wrong recommendations.

The fix is the AI operating system approach: one system that sees pricing, ranking, and margin across all your channels simultaneously, knows about Amazon's scraping behavior, and routes pricing decisions through the channel-architecture rules you set up. The Profasee pricing approach handles this directly.

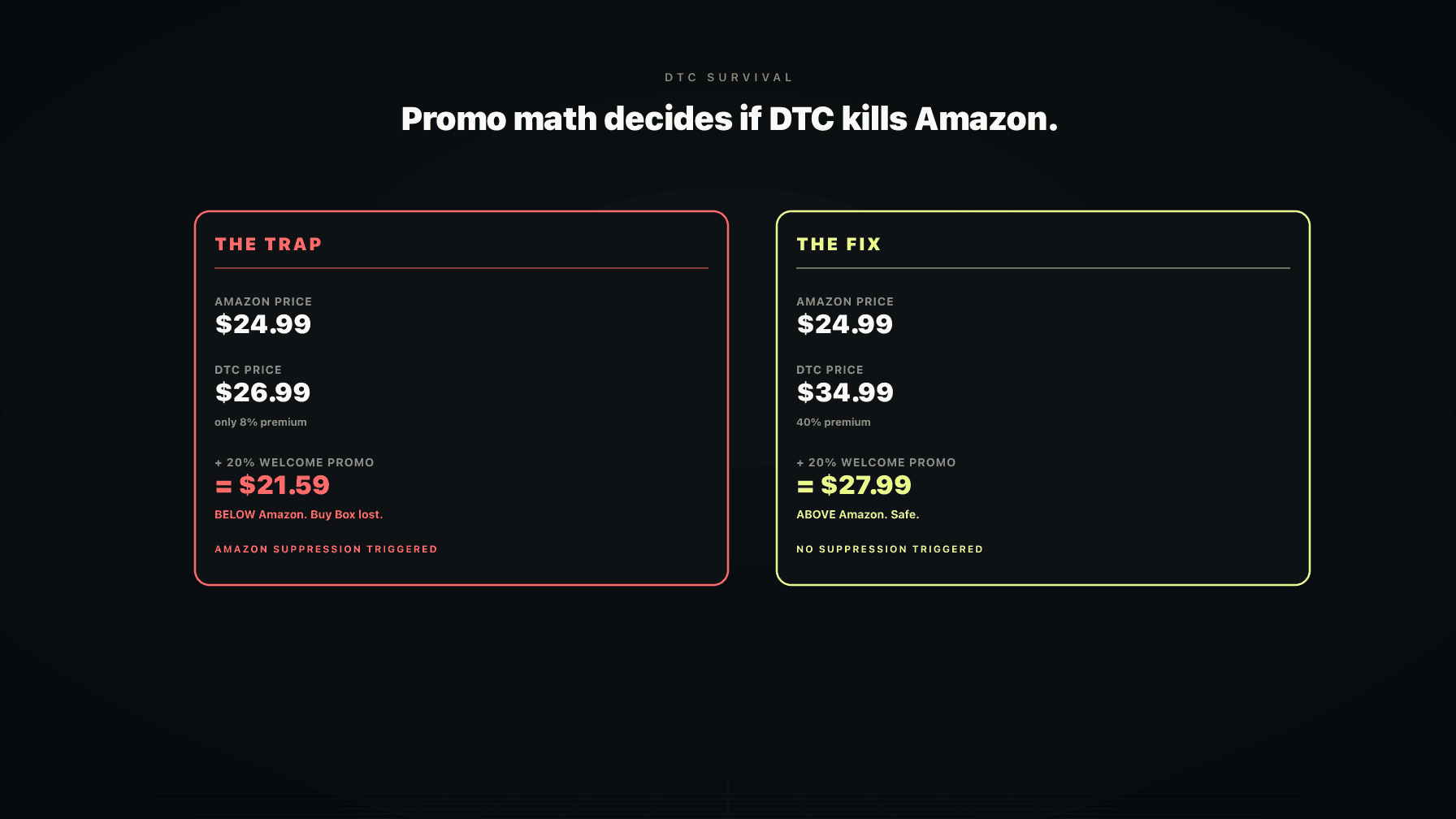

DTC sites are the most common version of this problem because brands set up Shopify with their full retail price (often higher than Amazon) and assume that is a separate transaction. It is not, from Amazon's perspective. Amazon scrapes the DTC site too. If your DTC price is higher than Amazon, that is fine (Amazon is happy to be the lower-price option). If your DTC has a "20% off welcome offer" that drops the effective price below Amazon, you have the same trap as the Walmart case, just from a different direction.

The DTC survival playbook covers how to run DTC alongside Amazon without creating the trap. The short version: your DTC site needs to either be priced above Amazon by enough margin that promotions do not drop it below, or be using different SKUs/bundles than Amazon entirely. Hybrid approaches usually fail.

If you are sitting on a brand that has already expanded multi-channel and you have never thought about this, here is the audit to run this week.

If you have not expanded multi-channel yet but are considering it, the framework runs in reverse. Decide which Move is right for your brand and your operational capacity before you list a single SKU off Amazon. Doing the architecture work up front is cheaper than untangling the mess later.

There is a deeper point underneath the tactical mechanics. Most operators think of channel expansion as a revenue question (how do I add a new revenue stream) when it is actually a margin question (how do I add a channel without damaging the margin on my existing channel).

The revenue framing puts you in a position where every new channel feels like progress because revenue went up. The margin framing puts you in a position where you actually evaluate whether the new channel is net-positive for the business, accounting for what it did to the channel that was already working.

This is the Steward of Capital frame applied to channel architecture. Revenue is vanity. Total contribution margin across all channels is the only number that matters. A "successful" Walmart expansion that dropped Amazon contribution margin by more than Walmart added is not a success. It is a failure that the revenue dashboard hid.

The deep-dives below take this framework apart in detail:

Read whichever one solves the problem in front of you. The architecture decision is one of the highest-leverage operator moves you will make in 2026.

It depends on whether the off-Amazon channel is defensive or offensive. Defensive (insurance against Amazon suspension or fee changes) calls for identical-pricing expansion or no expansion. Offensive (real second business) calls for different-SKU or different-brand expansion. The wrong move is the one most brands make: same UPC, different price per channel, which turns the smaller channel into your Amazon ceiling.

Yes. Amazon's pricing systems scrape Walmart, Target, your DTC site, and most other public marketplaces continuously. When it finds the same product at a lower price elsewhere, it suppresses your Buy Box, sends pricing notifications, or quietly downgrades your organic rank. This is the structural reason most multi-channel expansions hurt Amazon margins.

The 5% rule is the threshold at which a small channel becomes large enough to be visible to Amazon's pricing systems. Below 5% of revenue, the off-Amazon channel is usually invisible to Amazon's scraping. Above 5%, it shows up and becomes a factor in your Amazon Buy Box and ranking. The 5% rule deep-dive walks the mechanics.

Three ways. Hold identical prices across both channels. Use a different UPC on Walmart than on Amazon (different pack size, different bundle, different SKU). Or build a separate brand for Walmart. Same-UPC, different-price-per-channel is the trap that causes the Buy Box loss.

More expensive, by enough margin that any promotional discount on DTC does not drop the effective price below Amazon. If your DTC welcome offer is "20% off" and that drops the price below Amazon, Amazon's systems treat the discounted price as your real DTC price and you have the same trap as the Walmart case.

It is the structural problem where a small off-Amazon channel ends up dictating your Amazon pricing because of how Amazon's price-scraping systems work. The brand becomes a slave to the smallest channel because that channel sets the price ceiling. The fix is structuring the expansion so the channels do not look like the same product to Amazon's systems.

You do not need a separate agent. You need agents that share a state across channels. A pricing agent that only sees Amazon will miss the Walmart trap. A pricing agent that sees both channels can prevent the trap from being created in the first place. This is one of the operator reasons to run an AI operating system rather than disconnected single-channel tools.

If you take one thing from this post, take this: channel expansion is an architecture problem, not a revenue problem. You are not adding a revenue stream. You are restructuring the way your brand exists across multiple systems that scrape each other. The brands that win at multi-channel are the ones that did the architecture work first.

If you want to talk about wiring an AI operating system that handles multi-channel pricing without creating the trap, apply here.