Chad Rubin

June 25, 2026 · 12 min read

Operator notes by email

Short, opinionated takes on AI agents, Amazon PPC, pricing, and inventory. No fluff. About once a week.

Every operator I have ever met assumes the same thing about channel strategy. The big channel sets the rules. The small channel is a side bet. You can experiment on the small one, take some chances, undercut on price to gain a foothold, and the big one keeps humming along untouched.

On Amazon, that is exactly backwards.

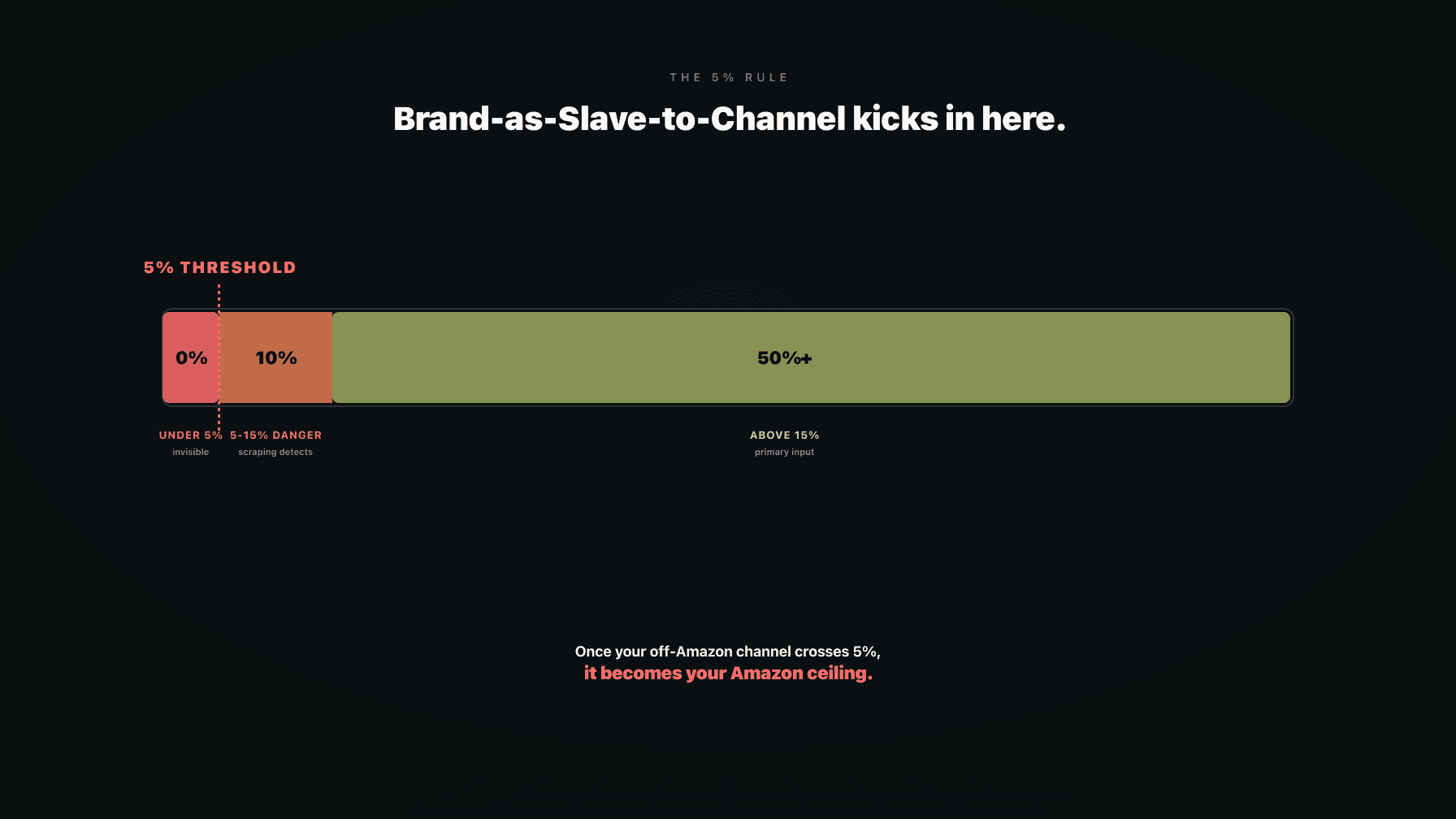

The smallest channel sets the rules. Amazon's algorithm is the most aggressive cross-channel price policer in commerce. It scrapes Walmart, Target, your own DTC site, your B2B portal, your eBay listings, every Shopify storefront with a UPC match. The moment a sibling channel goes live at a lower number, the clock starts. Once that channel hits roughly 3 to 5% of your total revenue, Amazon's pricing systems treat it as a real comparable, and that channel's price becomes the ceiling on your 95% channel.

This is what I call the Brand-as-Slave-to-Channel problem. The tail wags the dog. The 5% channel dictates the 95% channel, not the other way around. And most operators do not figure this out until their Amazon margin has already dropped by 20 to 30% and they cannot explain why.

I want to walk you through the mechanics. How the 5% threshold actually behaves. Why it is structural and not personal. The four ways Amazon will suppress you, ordered from silent to overt. What a real 200-SKU audit looks like in numbers. And the Monday-morning checklist for figuring out if you are already in the trap. If you are running a brand with serious Amazon exposure and any side channel of meaningful size, you need to understand this rule cold. Otherwise you are leaking money you cannot trace.

The 5% number is not a published Amazon policy. It is an inferred threshold that operators who run large catalogs across multiple marketplaces see in the data over and over. There are three regimes, and the math behind each one explains the inflection.

Regime one: below 5% of revenue. Amazon's scrapers see the channel. They have known about your Walmart listing or your DTC storefront since the day it launched. But the volume signal is too weak to act on. Amazon's pricing algorithm has to decide what is a real comp and what is noise. A storefront moving 50 units a month on the same UPC is noise. The cost of false-positive matching, suppressing your Buy Box, demanding a match on a phantom comp, is higher than the cost of letting it slide. So they let it slide. You can usually run a small DTC site at any price you want and nothing happens on Amazon. This is the "fine in pilot, broken at scale" zone, and it is the zone that lulls operators into a false sense of safety.

Regime two: 5 to 15% of revenue. This is where the algorithm flips. The off-channel is now a real comp. It has enough volume that a price discrepancy looks like a meaningful pattern of you charging Amazon customers more. The algorithm starts feeding the off-channel price into the Buy Box eligibility check and the Featured Offer logic. You will see soft suppression first. The Buy Box flickers. Then you get an email asking you to match the lower price elsewhere. If you ignore it, the suppression goes hard. Listing becomes ineligible for the Buy Box entirely, organic rank starts sliding, and conversion craters. The progression from soft to hard usually takes 30 to 60 days.

From reading to action

If the framework above sounds familiar, your Amazon account is probably carrying the same drag. Apply and we will show what Marko, Oracle, and Bruno would change in your first week.

Ran a 7-figure Amazon brand for a decade. Founded Skubana (acquired). Co-founded Prosper Show. 15+ years on Amazon.

Join the brands that replaced agencies and tools with AI employees.

Regime three: above 15% of revenue. The off-channel is now a primary input into the algorithm's pricing assessment, not just a comp. At this point Amazon does not just want you to match. It wants you to set Amazon as the lowest channel, period. If you refuse, you are functionally locked out of growth on the listing. Your ads will still spend, but the conversion rate will not support them. I have walked into operator P&Ls in this zone and the founders genuinely do not understand why their numbers cratered six months ago. The reason is the 8% Walmart play that went from 2% of revenue to 18% of revenue.

I wrote about the same pattern from a different angle in the multi-marketplace trap and in how Amazon scrapes Walmart and Target pricing in real time. The scraping is constant. The threshold is when it bites.

Here is the pattern, played out over and over across hundreds of brands I have looked at since 2010.

Year one, you launch on Amazon. You learn the platform, you survive the first inventory cycle, you figure out PPC. Year two, the brand starts working. You are doing real revenue, maybe $3 to $8 million on Amazon. Now you want to diversify. Everyone tells you not to be a one-channel brand, and that advice is correct in spirit. The execution is where it goes wrong.

You expand to Walmart. Walmart's referral fees are lower than Amazon's. Your 3PL costs are lower. So your contribution margin per unit is higher at the same price. The natural move, the move every spreadsheet tells you to make, is to lower price on Walmart to gain share. Maybe 8% off Amazon. Maybe 12%. You are still making the same margin you make on Amazon, because the cost structure is leaner, and the lower price wins the share.

For three to six months, this works beautifully. Walmart revenue climbs. Amazon revenue stays flat. Total revenue grows. You feel diversified.

Then Walmart hits 5% of total revenue. The algorithm flips.

What happens next is the Brand-as-Slave-to-Channel moment. Amazon suppresses Buy Box on the SKUs that have the Walmart discount. You investigate, find the price difference, and now you have a choice. Either pull the SKU off Walmart (lose the diversification), or lower Amazon to match Walmart (lose the margin on 95% of your revenue). Most operators lower Amazon. They cannot stomach pulling the channel they just built.

The smaller channel, the 5% channel, now dictates the price ceiling on the bigger channel. You are no longer a brand operating in a portfolio of channels. You are a slave to the lowest-price channel in your mix. The lower the price you set anywhere, the lower the price you can set on Amazon. The math gets uglier from here because Walmart's relative profitability looked attractive in isolation, but when you net out the Amazon margin loss across the 95%, the diversification play destroys total profit. I walk through this math in detail in the channel conflict math and from a margin protection angle in running off-Amazon channels without breaking margins.

When the algorithm flips at the 5% threshold, the suppression does not arrive in one obvious notification. It comes in four waves, ordered from silent to overt. By the time you notice wave four, waves one and two have been chewing through your P&L for two months.

Wave 1: Buy Box suppression (silent). Amazon quietly drops your Buy Box win rate on the affected ASINs. You still appear on the listing, but the orange button now lives with a different seller, or the listing displays the "See All Buying Options" link instead of a clean buy flow. No email, no warning. The drop is usually 15 to 30% in the first 14 days. This is wave one because most operators do not have Buy Box monitoring set up at the ASIN level, so it goes undetected.

Wave 2: Pricing notifications demanding match (overt). Now Amazon gets explicit. You get a Seller Central message: your listing is priced higher than [retailer], please update to remain eligible for the Featured Offer. This is the polite version. Operators read it and treat it as a soft suggestion. It is not. It is the algorithm telling you the suppression in wave one is about to get worse if you do not act.

Wave 3: Organic rank degradation (invisible until 60 days later). This is the wave that ruins quarters. Once Buy Box win rate drops, conversion rate on the listing drops with it. Amazon's organic ranking algorithm uses conversion rate as a primary input. So a lower Buy Box rate degrades rank, lower rank degrades impressions, lower impressions degrade sales, and the listing starts a slow spiral that does not bottom out for 8 to 12 weeks. The ugly part: even after you fix the price match, the rank does not snap back. You have to rebuild it through PPC and external traffic, which costs real money.

Wave 4: Conversion drop from lost Buy Box (compounds). When a customer lands on a listing without a clean Buy Box, conversion drops 40 to 70% versus the same listing with the Buy Box. This compounds with wave three because lower conversion makes PPC less efficient, ACoS goes up, and any ad-driven growth flywheel stalls. You are spending more per sale and getting fewer sales per dollar. The wave-four operator is the one who hires me and says "everything was working fine four months ago and now nothing works." It was the 5% rule.

The full pricing logic that drives all four of these waves is in the Amazon pricing strategy guide. The algorithmic context for why it is so unforgiving in 2026 is in the AI operating system frame.

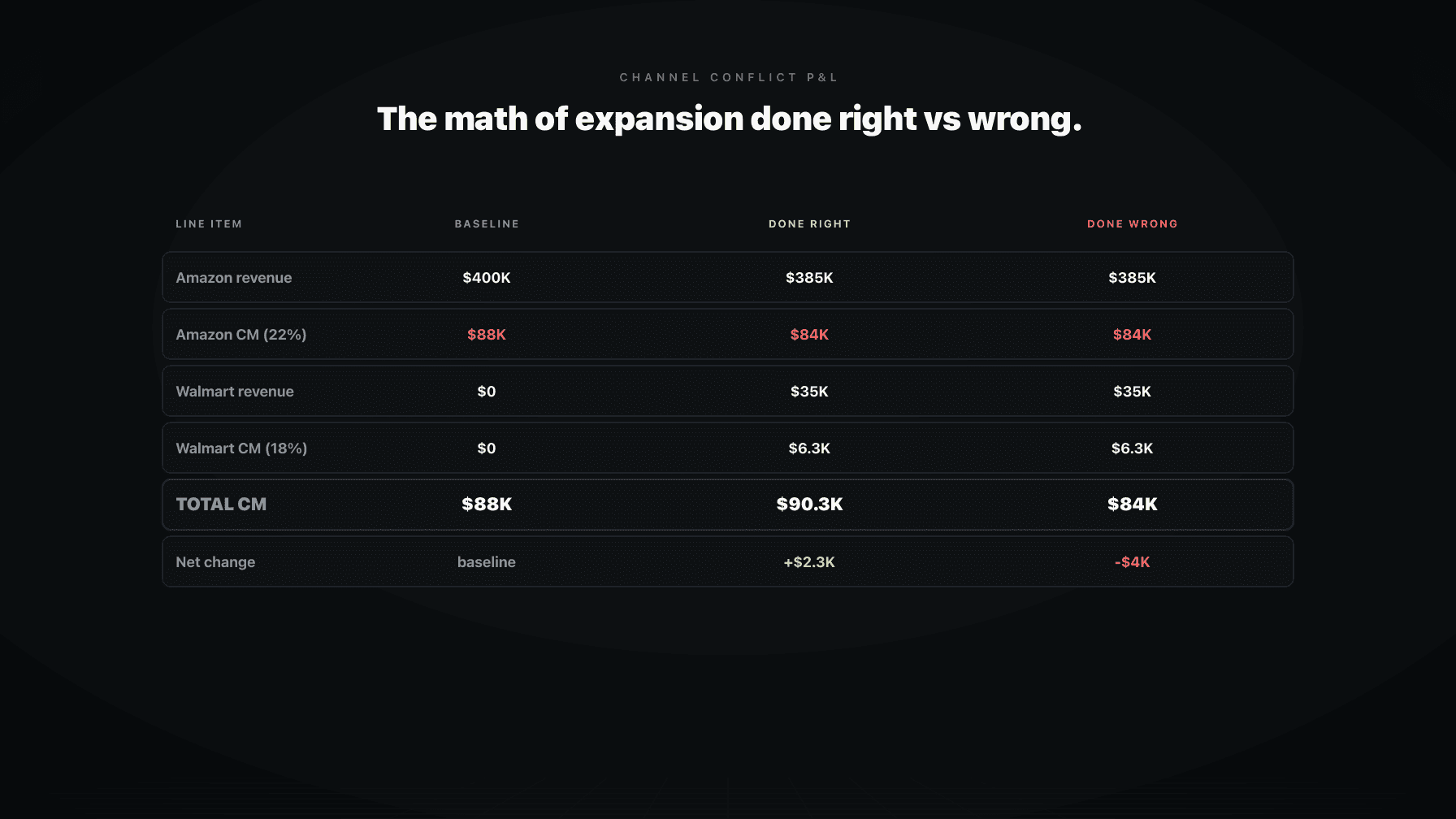

Let me make this concrete with a typical audit. The brand: 200 ASINs on Amazon, $14 million in trailing 12-month Amazon revenue, contribution margin around 22%. Founders decide to diversify and list their top 5 ASINs by revenue on Walmart, priced 8% below Amazon to drive Walmart share. Those 5 ASINs represent about $4.2 million of the Amazon revenue, so they are the SKUs where price match suppression hurts the most.

Here is what the next 60 days looked like in the audit data.

Buy Box win rate on the 5 ASINs: dropped from 94% average to 72% average. A 22-point drop. The other 195 ASINs were untouched.

Amazon revenue on those 5 ASINs: dropped 31% over the 60-day window. Some of this is Buy Box loss, some is rank degradation flowing through.

Walmart revenue on those 5 ASINs: gained roughly $4,000 per month. Real diversification, real revenue, but the absolute dollar gain was modest.

Amazon margin lost on those 5 ASINs: roughly $11,000 per month. The combination of revenue loss plus elevated PPC spend to defend rank ate the margin twice.

Net P&L impact: negative $7,000 per month, growing. The brand was poorer for having "diversified."

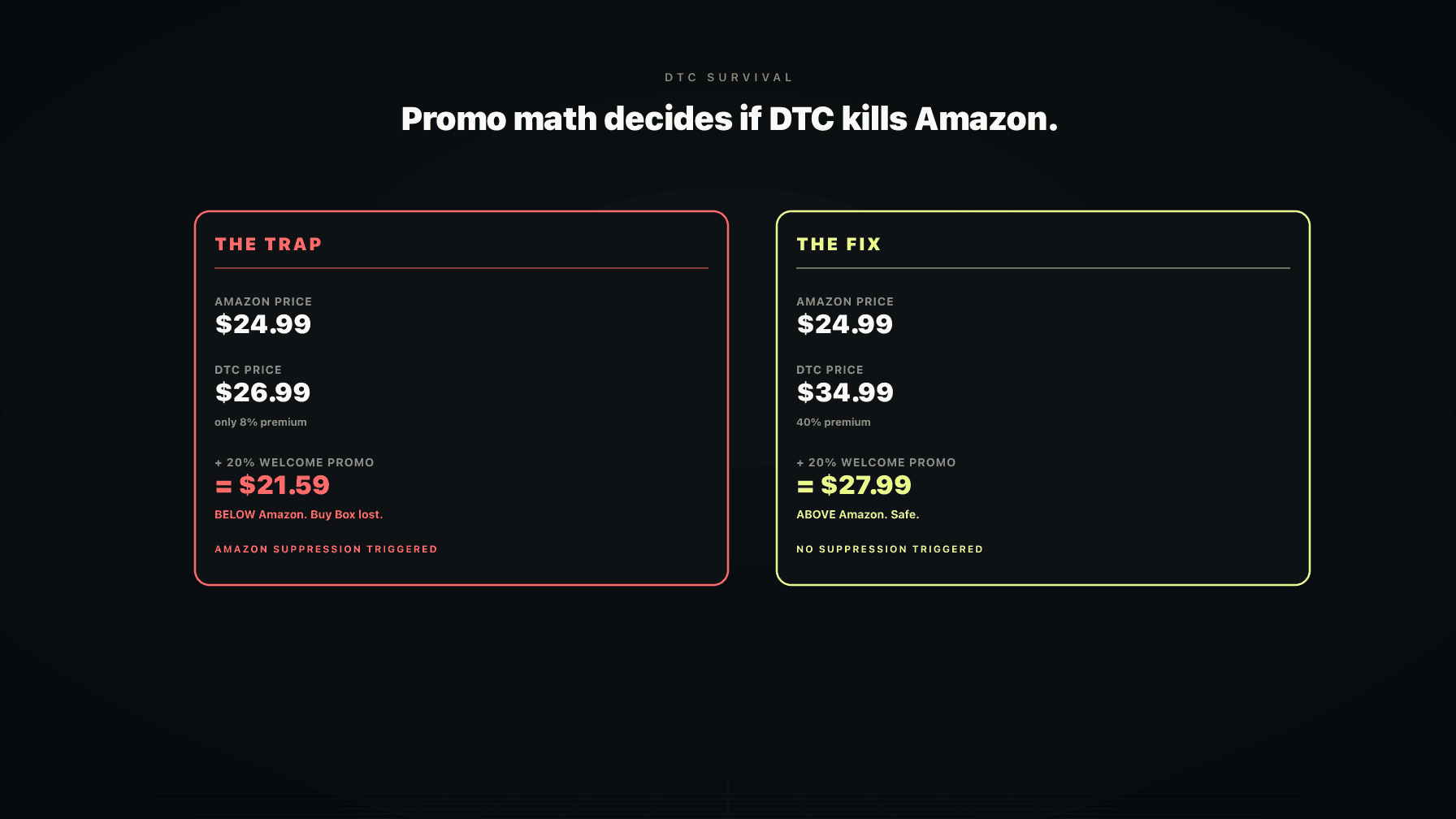

The founders did not see it until I ran the audit. They saw Walmart growing and assumed the Amazon dip was seasonal. They were running a profitable Walmart channel that was actively destroying their Amazon business. This is the math that the Brand-as-Slave-to-Channel framework predicts every single time. The relationship is structural. If you want to see the same numbers applied to a DTC site instead of Walmart, the DTC survival playbook for Amazon-first brands covers that variant.

This is the Monday-morning audit. Four steps. You can finish it before lunch if you have the data ready.

Step 1: Pull your top 20 ASINs by revenue. These are the SKUs that matter. If you have channel conflict on a tail SKU, it does not move the P&L. If you have it on a top-20 SKU, it is destroying you.

Step 2: Pull current pricing across every channel for those 20 ASINs. Amazon, Walmart, Target, your DTC site, eBay, any other live channel. Same UPC, same configuration, same pack size. Put it in a spreadsheet with one row per ASIN and one column per channel.

Step 3: Flag any ASIN where the off-Amazon channel price is below the Amazon price. Any gap, not just large ones. Even a 3% discrepancy is enough to trigger the suppression cascade once the off-channel hits volume. Flag color-coded by size of gap and by how much revenue that channel is doing as a share of total.

Step 4: Pull Buy Box win rate and organic rank trend on the flagged ASINs over the last 90 days. Look for the wave-one signal. If Buy Box win rate is trending down and you have an off-channel price gap, you are already inside the suppression cascade. If organic rank on the flagged ASINs is also degrading, you are in wave three.

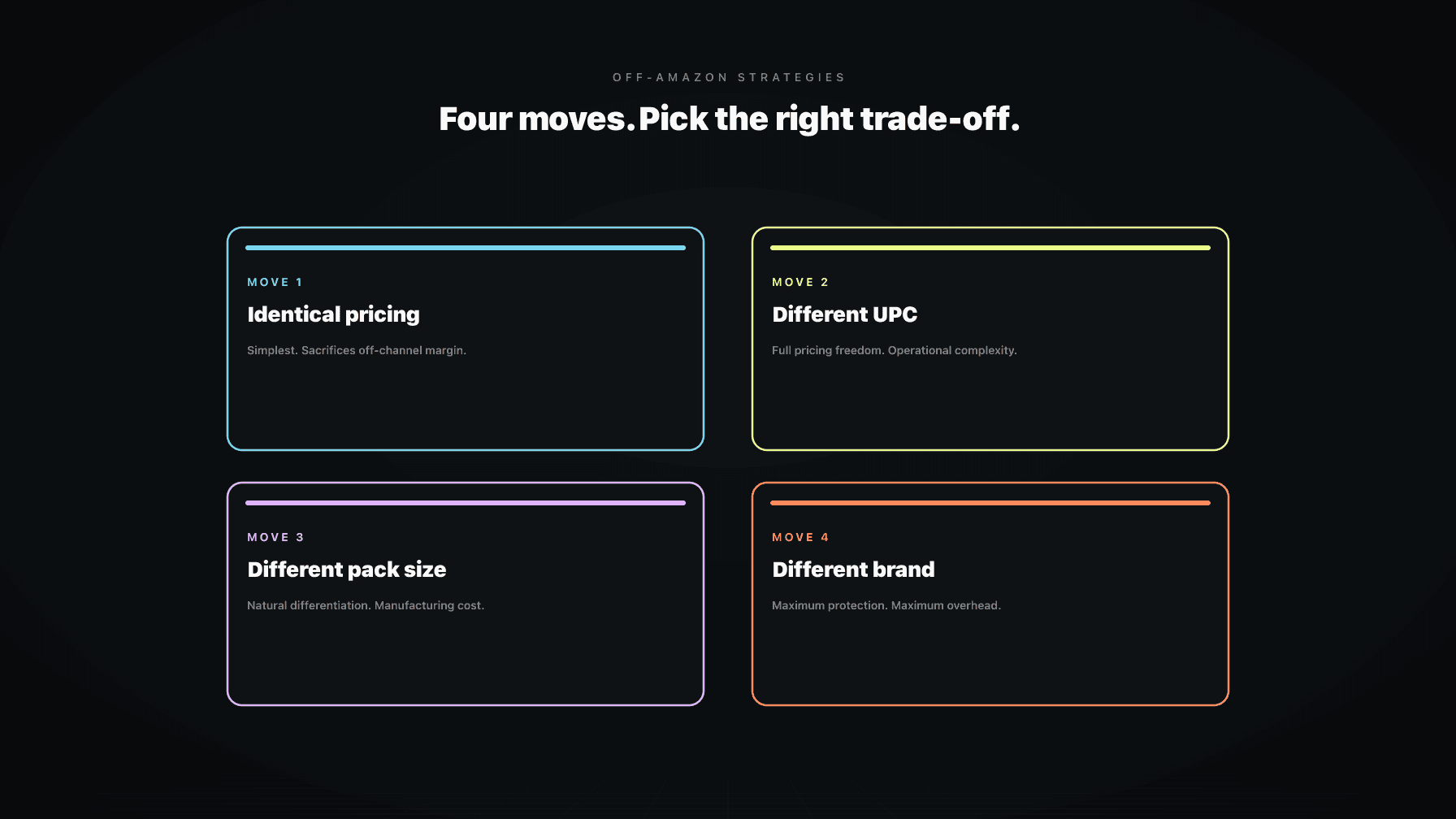

If steps three and four light up red, you have two real options, not three. Option one: raise the off-channel price to match Amazon, accept the lost share on the side channel, recover Buy Box and rank on the main channel. Option two: change the product configuration on the off-channel (pack size, bundle, variant) so the UPC no longer matches and the price comparison breaks. The third option, lower Amazon to match, is the trap. It feels like the cheap fix and it permanently lowers your blended margin across 95% of your revenue. The framing for thinking about this trade is in the steward of capital frame and the broader market cycle is in the Amazon capital cycle for 2026.

It is tempting to read this whole essay and conclude that Amazon is hostile. That is the wrong frame and it will lead to bad decisions.

Amazon is doing exactly what its customer-obsession algorithm is built to do. From Amazon's perspective, you are selling the same product cheaper on another channel. That means Amazon customers are paying more for the same item. The algorithm treats this as a customer experience violation. It does not care that you have different cost structures, different fee schedules, different marketing math, or different strategic reasons for the price gap. It only has one signal: same product, cheaper somewhere else. From that signal, the only correct action is to either lower the Amazon price or stop featuring your offer.

The 5% rule is structural because it falls directly out of that logic. Below 5%, the signal is noisy. Above 5%, the signal is reliable. The algorithm acts on reliable signals.

If you internalize this, the strategic implication is clear. You do not fight the algorithm. You design around it. You either keep your off-channel pricing at or above Amazon, or you structurally break the UPC match so the comparison cannot be made, or you accept that the off-channel will permanently dictate your Amazon ceiling. Picking one and committing is the operator move. Pretending the rule does not exist is the move that destroys quarters.

If you want a team that can actually run this audit on your full catalog every week and route the right pricing decision to the right channel without you babysitting it, apply here. That is what we built. The 5% rule is not going away. The brands that survive 2026 are the ones who designed for it instead of getting blindsided.

The 5% rule is the inferred threshold at which Amazon's price scraping systems start treating an off-Amazon sales channel as a real pricing comparable. Below roughly 5% of your total revenue, an off-channel can run at a different price without triggering algorithmic action on your Amazon listing. Above 5%, Amazon begins suppressing the Buy Box, sending price-match demands, and degrading organic rank if the off-channel is priced lower. The smaller channel effectively dictates the pricing ceiling on the larger channel, which is what I call the Brand-as-Slave-to-Channel problem.

Yes, continuously. Amazon has run cross-marketplace price comparison since at least the mid-2010s and the systems have only gotten more sophisticated. They match on UPC, brand, model number, and image hash. Walmart, Target, Best Buy, Home Depot, Wayfair, eBay, and major DTC platforms are all in the scrape set. The detailed mechanics are in the price scraping breakdown.

The scrape is constant, so detection itself is essentially real-time. What takes time is the algorithmic decision to act. From the moment your off-channel hits the volume threshold, the first wave of Buy Box suppression typically arrives within 14 to 30 days. Pricing notifications follow within 30 to 45 days. Organic rank degradation shows up at 45 to 90 days. Plan your timeline assuming a 30-day reaction window from the algorithm.

Sometimes, if you do it structurally. Different shipping speeds alone are not enough; Amazon's comp logic accounts for shipping. But genuinely different pack sizes, different SKU configurations, or different bundles with distinct UPCs will break the match. The key is that the products must look different at the UPC and listing level, not just on the marketing page. If you ship the same UPC to Walmart at a lower price and call it a bundle, the scraper will still match it and you will still get suppressed.

This is where many brands get blindsided. Walmart marks up your wholesale price by some margin, but if their final retail price still comes in below your Amazon price, you trigger the 5% rule on Amazon. Walmart sets the shelf price; you do not. The defense is either negotiating a minimum advertised price (MAP) clause with Walmart, which is hard to enforce, or selling a structurally different SKU into Walmart that does not UPC-match your Amazon catalog.

The cross-border version is softer because Amazon treats marketplaces (US, UK, DE, JP) as separate algorithmic environments. The scraping does not flow as aggressively across borders. However, if you sell on Amazon.ca and Amazon.com with the same UPC at meaningfully different prices, the US algorithm will eventually treat the Canadian listing as a comp once volume crosses the threshold. The rule still applies, the threshold just behaves differently across geographies.

Build a weekly cross-channel pricing dashboard for your top 20 to 50 ASINs. Track three things per ASIN: current price on every live channel, Buy Box win rate on Amazon, and organic rank position. Set an alert when any off-channel price drops below Amazon by more than 2%, and a second alert when any flagged ASIN's Buy Box win rate trends down for more than 7 days in a row. Most operators do not have this dashboard. If you would rather have a team running it for you continuously instead of building it yourself, apply here.