Chad Rubin

June 17, 2026 · 12 min read

Operator notes by email

Short, opinionated takes on AI agents, Amazon PPC, pricing, and inventory. No fluff. About once a week.

Amazon is a market. Markets move in cycles. Every other capital market on the planet (equities, real estate, venture, even consumer credit) gets analyzed through a cycle framework, because a cycle framework changes the question from "how do I grow?" to "should I be playing offense or defense right now?" Amazon does not get that treatment, mostly because the people writing about Amazon are not capital allocators. They are sellers, agencies, and influencers who talk tactics for whatever phase they happen to be living in.

That is the gap this post fills. I have been running and operating on Amazon for 15 years. I have lived through three of these cycles. I sold Skubana in one phase, watched the aggregator boom and bust happen in the next, and I am sitting in front of the current phase right now. After enough cycles you stop reading the market as a stream of headlines and start reading it as a wave you can predict, position for, and exploit.

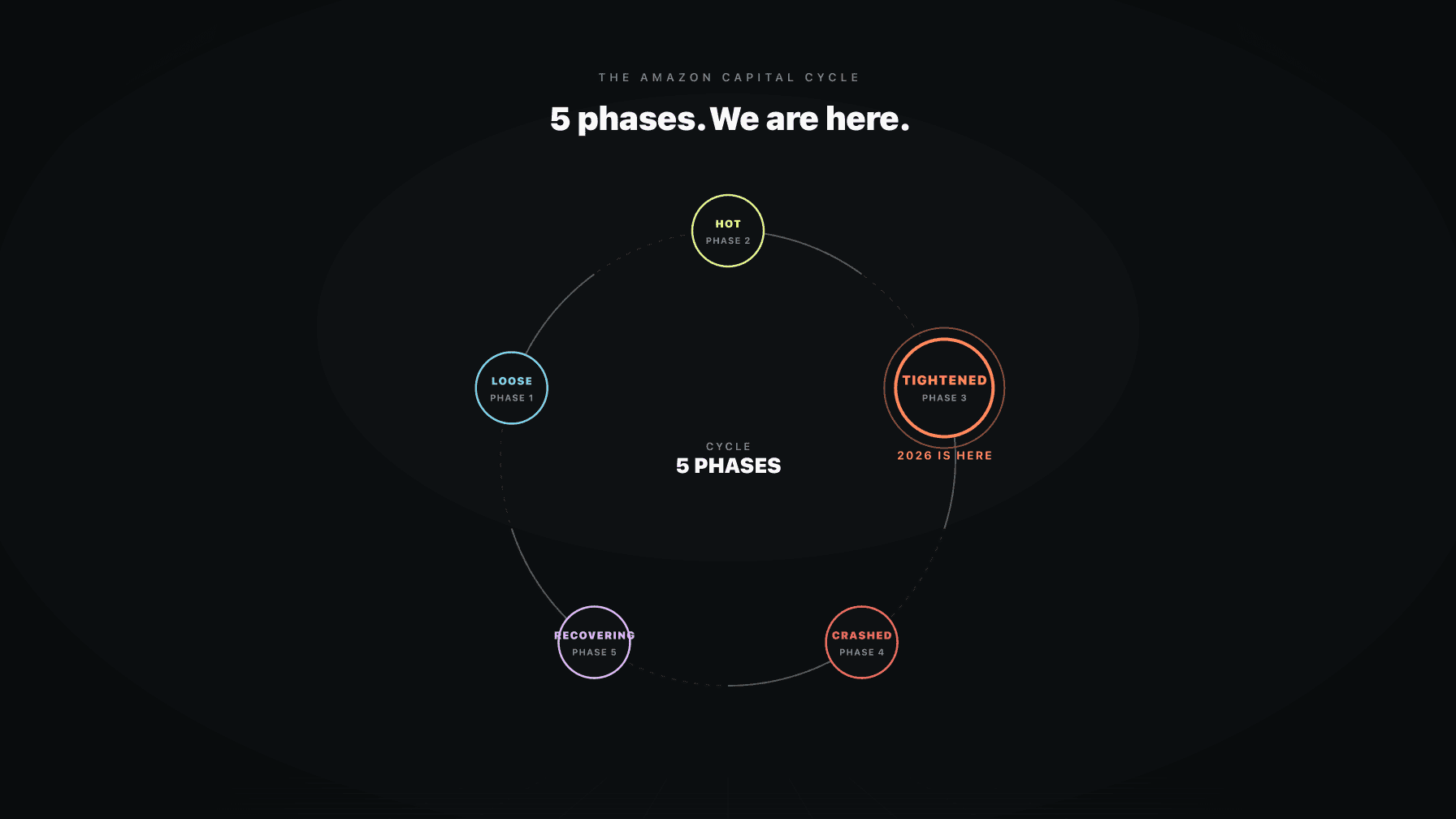

I call it the Amazon Capital Cycle. Five phases. Loose, Hot, Tightened, Crashed, Recovering. Each phase has a clear set of characteristics, and each phase requires a different operating posture. The brands that survive cycles do not have better tactics than the ones that die. They read the phase correctly and pivot the operating posture before the rest of the market catches on.

In 2026 we are deep in the Tightened phase. This post explains what that means, what is coming next, and what an operator should be doing about it right now.

## Key takeaways >- Amazon moves through five capital phases like any other market: Loose, Hot, Tightened, Crashed, Recovering.- In 2026 we are in the Tightened phase: capital scarce, sellers reducing inventory, market consolidating, pessimism at all-time highs.- The Tightened phase rewards lean operations, profit discipline, and cross-functional coordination. It punishes growth-at-all-costs, agency dependence, and disconnected tools.- Most operators read the Tightened phase as a problem. The brands that win read it as the best buying and consolidation opportunity in a decade.- The phase after Tightened is Crashed, then Recovering. Positioning now decides what your brand looks like when the next Hot phase arrives.

The reason a cycle framework changes the conversation is that the right tactic in one phase is the wrong tactic in another. Aggressive ad spend that compounds organic rank is right in a Hot phase and catastrophic in a Tightened phase. Holding inventory deep into seasonality is right in a Loose phase and a margin grave in a Tightened phase. Buying a competitor brand at a 5x multiple was the move in 2021. The same brand at a 5x multiple in 2026 is overpaying for distress.

Operators who get the phase right outperform the average operator by a multiple, not a margin. That is the size of the prize for reading the cycle correctly.

From reading to action

If the framework above sounds familiar, your Amazon account is probably carrying the same drag. Apply and we will show what Marko, Oracle, and Bruno would change in your first week.

Ran a 7-figure Amazon brand for a decade. Founded Skubana (acquired). Co-founded Prosper Show. 15+ years on Amazon.

Join the brands that replaced agencies and tools with AI employees.

The most common mistake is operating in a phase you used to be in. The brand that learned its tactics in the 2021 Hot phase and is still running those tactics in 2026 is the brand whose margins look terrible right now. Not because the operator is bad. Because the operator is playing the wrong phase.

I will give the full mechanics of each phase in the five-phases deep-dive post. Here is the operator-level summary.

Capital is cheap. Inventory is easy to finance. New sellers enter the marketplace daily. Competition is rising but margins are still defensible because demand is growing faster than supply. Aggregators are raising funds. Multiples are climbing.

The signal: capital allocators talking publicly about "the Amazon roll-up opportunity." Multiples for healthy Amazon brands above 4x EBITDA. Inventory financing readily available. The phrase "growth at all costs" sounds reasonable.

The right tactic: grow. Stake category positions. Acquire keywords. Build SKU depth. The cost of capital is low and the cost of being absent is high.

This is the boom. Aggregators are paying 6 to 8x EBITDA. Sellers raise capital easily. Every category looks crowded but every brand is still profitable because demand is still outrunning supply. PPC costs are climbing but ROI is still positive because conversion holds.

The signal: mainstream press covering Amazon FBA as a wealth-creation story. Multiples for healthy brands at 6 to 8x EBITDA, sometimes higher. The phrase "everyone is winning" sounds true. New sellers entering with no operational experience and getting away with it.

The right tactic: sell, raise, or consolidate aggressively. This is the phase where the smart capital exits. The Hot phase ends without warning. Brands that took the offer in 2021 are happy today. Brands that held out for "next year's multiple" are not.

Capital tightens. Inventory financing dries up. Sellers reduce inventory to free up cash. Market consolidates. Margins erode. PPC costs hold or rise while conversion drops. Aggregators stop buying. Brands that survived on cheap capital and growth narrative die in the open.

The signal: sellers complaining about Amazon fees and margin compression. Aggregators going quiet or filing for restructuring. Multiples for healthy brands compressed to 2 to 4x EBITDA. The phrase "Amazon is dead" trending on operator Twitter.

The right tactic: play lean. Cut spend that does not produce profit. Coordinate decisions across functions to eliminate the silos that bleed margin (this is what the AI operating system is built for). Treat yourself as a steward of capital, not a revenue chaser. Buy distressed assets carefully if you have the operational chops.

This is also the phase where the best operators consolidate. Distressed brands are everywhere. The brands that have the operational muscle to turn around an underperforming asset can buy at 2x EBITDA and ride the Recovering phase up.

The phase that comes after Tightened, usually within 6 to 18 months. Insolvencies accelerate. Forced exits hit the market. Multiples for healthy brands stay compressed and multiples for unhealthy brands go to zero. Tools and software companies in the space consolidate or die.

The signal: aggregator bankruptcies in the press. Public distress sales. The phrase "buying opportunity of the decade" starting to show up from sober capital allocators. Brands shutting down quietly because the unit economics no longer work.

The right tactic: if you have capital and operational chops, buy. If you do not, survive. The brands that emerge from the Crashed phase with intact margins and growing rank are the brands that own the next Hot phase.

Multiples start expanding again. Survivors are stronger than they were going into the Tightened phase, because they were forced to operate lean. New capital comes in cautiously. Demand stabilizes. Aggregators of a different shape (smaller, sharper, more operationally focused) emerge.

The signal: healthy brands trading hands at 4x EBITDA again. Capital allocators returning to the category. The phrase "the next wave" appearing in industry coverage. New tools and platforms launching with serious operational chops.

The right tactic: grow again, but smarter than last time. The brands that get to this phase with cash, infrastructure, and reputation are the ones that build the next decade's category-leading brands.

Every indicator that defines the Tightened phase is present right now.

Capital tightened: interest rates moved in 2022 and never came back to the cheap-money baseline of 2021. Inventory financing that was easy in 2021 is hard in 2026. Inventory factoring rates are up. SBA loans for Amazon brands are harder to get than they have been in a decade.

Sellers reducing inventory: Amazon has been raising fees, particularly storage and fulfillment fees, which has pushed sellers to carry less inventory. Days-of-cover for the average Amazon brand has compressed. Out-of-stocks are up year over year. The brands holding a lot of inventory are getting margin-squeezed by Amazon's own fee structure.

Market consolidating: aggregators that were buying brands at 6x EBITDA in 2021 are either restructuring, selling portfolios, or quietly disappearing. The brands they bought are being unwound at discounts. Operational brands that stayed independent are absorbing customers and SKUs from the unwinding aggregators.

Pessimism at all-time highs: if you spend any time in the Amazon-seller corners of the internet, you know the dominant tone. "Amazon is dead." "Margins are gone." "FBA does not work anymore." This is exactly how late-Tightened looks before the Crashed phase begins.

Multiples compressed: brands that would have traded at 6x EBITDA in 2021 are trading at 2 to 4x EBITDA now. Multiples for unhealthy brands are at zero. There is no aggregator demand pulling multiples up, and the strategic buyers who are still active have learned to be patient and demanding.

The Tightened phase has been running for roughly 18 months in 2026. Historically Tightened lasts 18 to 30 months before tipping into Crashed. That puts the next phase between Q4 2026 and Q2 2027.

This is the part most posts about "the state of Amazon" miss. The phase tells you what is happening. It does not tell you what to do. Here are the four operator postures that work in Tightened, ranked by leverage.

This sounds obvious. It is not. Most Amazon brands in 2026 are still running PPC campaigns that lose money, paying agencies that produce no measurable lift, and holding inventory in categories whose unit economics no longer work. The Tightened phase rewards ruthlessness about profit. Every dollar of expense gets justified by a dollar of margin. The unit economics post is the math.

The hardest cut for most operators is the agency cut. A $10K/month operational agency that produces $3K of measurable lift was acceptable in the Hot phase. In Tightened it is the most leveraged cost on the P&L. The math is brutal and the math is right.

The Tightened phase exposes every silo in your operation. A PPC tool that does not see inventory is wasting spend on stockouts. A repricer that does not see margin is racing competitors to the bottom. A demand planner that does not see ad spend is forecasting on the wrong demand signal. In a Loose phase these silos are expensive but tolerable. In Tightened they are fatal.

This is the operator case for an AI operating system approach over disconnected single-function tools. The brands that emerge from Tightened in good shape are the ones whose decisions coordinate across functions automatically. The brands that emerge wounded are the ones whose tools never talked to each other.

In Loose and Hot, your job is to generate revenue. In Tightened, your job is to generate revenue in relation to budget. The frame matters. A brand pushing for revenue growth in Tightened is the brand burning capital trying to outrun a cycle that will outlast the capital. A brand operating as a steward of capital is the brand still standing when the cycle turns.

The shift is reading your business like a CFO instead of like a marketer. EBITDA per ASIN. Contribution margin per unit. Days of cover. Cash conversion cycle. These become the numbers you operate against, not revenue and ACoS.

The Tightened phase is the start of a multi-year buying window for operationally capable brands. Distressed Amazon brands are everywhere in 2026. The aggregator unwind is producing forced sales. The independent sellers who ran out of capital are looking for buyers. The brands that bought too much SKU depth in the Hot phase are dumping inventory and listings at discounts.

This posture is only for operators with the operational muscle to actually turn around an underperforming asset. The distressed Amazon businesses post covers the diligence framework. Most buyers in this phase will lose money because they will underestimate the operational lift required. The few who get it right will own categories.

Two structural shifts make the 2026 Tightened phase materially different from the 2008 or 2015 squeezes.

First, the operating leverage from AI is real. Brands that ran on 8 employees in 2021 are running on 3 employees in 2026, doing more volume, with higher margins. The revenue-per-employee frame is the operator's new flex. Brands that have not made this shift are competing against ones that have, and the math does not work for the unbundled side.

Second, Amazon's own cost structure is squeezing. Fees have been rising for three years and the rise is structural, not cyclical. CRaP (Can't Realize a Profit) is no longer just a problem on $5 commodity items. CRaP is now squeezing $25 products in dense categories. The brands that win the next phase will have unit economics that survive Amazon's continued fee increases. The brands that do not will be cleared out regardless of operator skill.

The base case for the next 12 months is that Tightened continues, with growing pockets of Crashed. The Crashed phase will be visible by Q4 2026 in some categories and Q1 2027 in most others. The Recovering phase historically takes 12 to 24 months to fully form, which means the next Hot phase is a 2028 event at the earliest.

Operator implications:

The Amazon Capital Cycle is a five-phase framework I have used for 15 years to read where the marketplace is and what operating posture the moment requires. In 2026 we are deep in Tightened, the next phase is Crashed, and the brands that win the next cycle will be the ones that read this phase correctly and operate accordingly.

The Amazon Capital Cycle is a framework I developed across 15 years of operating Amazon brands to read the marketplace through a five-phase capital lens: Loose, Hot, Tightened, Crashed, Recovering. Each phase has characteristic signals and requires a different operating posture. The cycle reframes the operating question from "how do I grow?" to "what phase is the marketplace in, and what should I be doing in this phase?"

Tightened. Capital is scarce, sellers are reducing inventory, the market is consolidating, multiples have compressed to 2 to 4x EBITDA for healthy brands, and operator pessimism is at multi-year highs. The Tightened phase has been running for roughly 18 months and historically tips into the Crashed phase between months 18 and 30, which puts the transition between Q4 2026 and Q2 2027.

Four operator postures work in Tightened. Cut everything that does not produce profit. Coordinate decisions across functions to eliminate silos. Operate as a steward of capital, not a revenue chaser. Consolidate distressed assets if you have the operational muscle. The brands that come out of Tightened in good shape are the ones whose unit economics are tight and whose decisions coordinate automatically.

The 2020 to 2022 aggregator model (raise capital, buy at high multiples, scale through finance rather than operations) is effectively dead. The next form of aggregation will be smaller, more operationally focused, and built around AI operating leverage rather than capital leverage. The why aggregators failed post covers what specifically went wrong and what the next iteration looks like.

For operationally capable buyers with cash and patience, yes. Multiples are compressed, distressed inventory is everywhere, and the Recovering phase is a 2027 to 2028 event. Buying carefully in Tightened and Crashed is the strongest setup for ownership in the next Hot phase. For undercapitalized or operationally weak buyers, the buying window is a trap, because turning around a distressed Amazon brand requires real operational lift.

Each phase tends to run 12 to 30 months, with the full Loose-to-Loose cycle typically running 5 to 8 years. The 2014 to 2018 cycle, the 2019 to 2022 cycle, and the 2022 to current cycle have followed roughly that cadence. Phases can shorten or extend based on macro factors (interest rates, e-commerce demand, Amazon policy changes), but the sequence is reliable.

The Amazon Capital Cycle is marketplace-specific. It is driven by capital availability, Amazon fee structure, seller competition, and demand patterns within the marketplace itself. A normal recession is a macroeconomic event. The two can correlate (the 2022 macro tightening coincided with the start of the current Amazon Tightened phase) but the Amazon cycle has its own internal logic and can move independently of the broader economy.

The brands that win the next decade on Amazon are not the ones with the best tactics. They are the ones reading the phase correctly and shifting their operating posture as the cycle turns. Tightened rewards lean, coordinated, profit-disciplined operations. Crashed rewards capital with operational chops. Recovering rewards the brands that survived the previous two phases with their unit economics intact.

The full operator playbook for the Tightened phase runs across this whole cluster. The aggregator post-mortem is what not to do. The brand valuation post is how to think about M&A in this phase. The distressed asset post is the buying framework. The steward of capital post is the operator mindset.

If you want to talk about wiring an AI operating system to your brand for the Tightened phase, apply here.